Why is My Mortgage Pay Out the Same as if I Continue Paying Regular Payments

Just about everyone with a home loan ponders the idea of paying a little extra, whether it's via biweekly mortgage payments, or just once a year after receiving a sizable bonus or tax refund.

Whatever the method, you should first consider why you're thinking about paying your mortgage off early as opposed to putting the money elsewhere.

This is a particularly important question to ask in the super-low mortgage rate environment we've been enjoying for some time.

Simply put, mortgage borrowing has been really cheap, and is probably the least expensive debt you've got, so prioritizing it over other debt may not make sense.

For example, if you have student loan or credit card debt, it might be more beneficial to pay that off first.

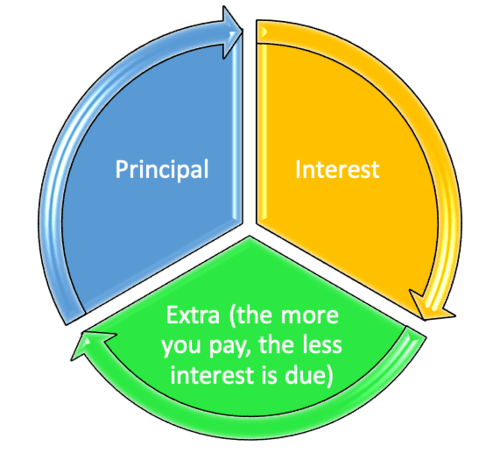

A Mortgage Is an Amortizing Loan with Equal Monthly Payments

- Most mortgages have a set loan term in which they are paid off in full

- Fully-amortizing payments consist of a principal and interest portion

- The monthly payment amount typically doesn't change unless it's an ARM

- But the portion that goes to principal/interest will adjust over time as your loan is paid off

Assuming you decide to make extra mortgage payments, whether significantly larger or just a little more than required, your next monthly payment won't change due to the previous payment.

You will still owe what you owed the month before, regardless of your principal balance being smaller.

While this might sound unfair, it all has to do with math and the fact that a mortgage is an amortizing loan.

Traditional mortgages are paid off over a certain set time period with regular monthly payments that consist of a principal and interest portion.

This total payment amount does not change (barring an ARM adjustment or negative amortization) regardless of whether you pay more than is due each month.

The only thing that changes over time is the composition of your mortgage payment, with the portion going toward principal increasing over time as the loan balance falls.

As more of the payment goes toward principal, less go toward interest – picture an old-fashioned balance scale where one side drops while the other rises.

Let's take a look at an example to illustrate:

Mortgage amount: $100,000

Mortgage interest rate: 5%

Loan type: 30-year fixed

Monthly payment: $536.82

In our example, your monthly mortgage payment would be $536.82 per month for 360 months.

The very first payment would allocate $416.67 toward interest and the remaining $120.15 would go toward principal.

This right here illustrates how interest on mortgages is front-loaded, with about 78% of the payment going toward interest and doing nothing to pay down the loan balance.

It also explains why so many homeowners want to pay off their mortgages faster. To save money!

To calculate the interest portion of the payment, simply multiply 5% by $100,000, and divide it by 12 (months). The principal portion is the remainder, as noted above.

For the second payment, you need to use an outstanding balance of $99,879.85 to account for the principal amount paid off via payment one ($120.15).

So to calculate interest for the second payment, you multiply $99,879.85 by 5% and come up with $416.17. This is the interest due and the remainder of the $536.82 payment goes toward principal.

Over time, the interest portion decreases as the outstanding balance decreases, and the amount that goes toward principal increases.

If You Pay More Each Month the Payment Composition Will Change, But You Won't See Immediate Relief

- While paying more than necessary won't lower the minimum amount due on your next mortgage payment

- It will change the composition of all future payments thanks to a lower outstanding balance

- This means you'll save on interest and reduce your loan term despite owing the same each month

- In other words paying extra is well-suited for those looking to save money long-term, not to obtain payment relief

If you make some additional payments toward your home loan, the outstanding loan balance will drop prematurely based on the original amortization schedule.

But instead of your subsequent monthly mortgage payments decreasing, the composition of your next payment (and the payment after that) will become more principal-heavy.

In other words, the payment due would still be $536.82 the next month (using our sample from above), but more of it would go toward principal (paying down your balance).

And for that reason, less interest would be paid throughout the life of the loan, and the mortgage would eventually be paid off ahead of schedule. These are the two benefits of making extra payments.

The less obvious downside is you wouldn't enjoy lower payments in the future, which could be an issue if money becomes unexpectedly tight.

For example, if you aggressively pay down your mortgage, you could find yourself in a house poor position.

Instead of reducing your monthly nut, more money is essentially locked up in your home until you either sell the property or refinance and pull equity (cash out refinance).

Recast or Refinance If You Want to Lower Future Mortgage Payments

- Paying extra today will NOT lower your next mortgage payment

- The only way future mortgage payments will drop is if you recast or refinance your loan

- Make sure you have ample reserves in the bank after making any extra payments

- The money could be trapped in your home and unavailable for other more pressing needs

If you made additional payments and want subsequent monthly payments to be lower, you have two options to get payment relief.

You can refinance the loan, which would also re-amortize the loan based on a brand new loan term.

Of course, if you're well into a 30-year loan, you'll reset the clock if you go with another 30-year term.

That's why it's recommended to go with a shorter term loan when refinancing such as a 15-year fixed mortgage, which kind of defeats the purpose of lowering monthly payments.

The other option you might have is to request a "loan recast," where the lender re-amortizes the loan based on the reduced principal balance.

This generally only makes sense if you make a sizable extra payment, something that would really change the payment structure of the loan.

In fact, some banks may only offer a recast it if you make a certain lump sum payment that cuts a certain percentage off the loan. They'll also charge you a fee to do it in most cases.

So while both a refinance and a recast can lower monthly payments, you have to be careful not to tack on more costs as you attempt to pay your mortgage down faster.

At the end of the day, it can be very worthwhile to make larger payments even if your subsequent payments don't change, just make sure you have money set aside for a rainy day.

Lastly, consider the fact that mortgages are often good debt, especially with the ultra-low rates many homeowners have locked in for the next 30 years.

Source: https://www.thetruthaboutmortgage.com/paying-more-today-wont-lower-future-monthly-mortgage-payments/

0 Response to "Why is My Mortgage Pay Out the Same as if I Continue Paying Regular Payments"

Post a Comment